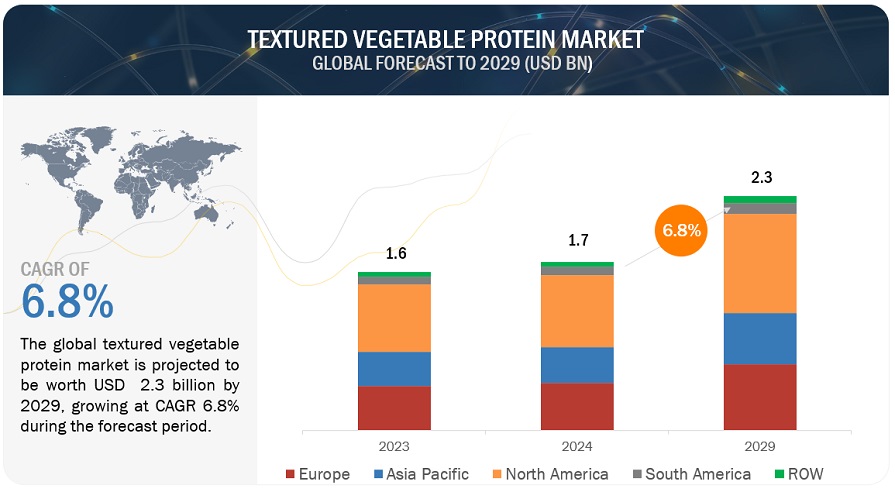

The textured vegetable protein market size is expected to grow from USD 1.7 billion in 2024 to USD 2.3 billion by 2029, representing a compound annual growth rate (CAGR) of 6.8% over the forecast period. This growth is fueled by increasing health, environmental, and ethical demands for plant-based diets, greater awareness of the nutritional benefits of vegetable proteins, a shift toward clean eating and natural ingredients, and a public focus on sustainable food production. Additionally, the versatility of textured vegetable proteins in mimicking meat’s texture and taste, along with their cost-effectiveness and long shelf life, makes them appealing for a variety of food products, including meat alternatives, snacks, and ready-to-cook meals.

Textured Vegetable Protein Market Drivers: Growing adoption of meat alternatives

The shift towards plant-based diets has been driven by concerns for the environment, animal welfare, and human health. This change in consumer preferences has led to a growing demand for meat alternatives that excel in taste, texture, and nutritional value compared to traditional meat products. Textured vegetable proteins, derived from sources like soy, wheat, and peas, play a crucial role in this trend. They are versatile ingredients used as meat substitutes and extenders in processed foods, including burgers and sausages. As food manufacturers continue to innovate and introduce new plant-based meal options to meet the rising demand, the potential for textured vegetable proteins is vast and ever-expanding.

Textured Vegetable Protein Market Opportunities : Expansion of foodservice industry

One opportunity for textured vegetable protein in the market is its use in foodservice. The increasing vegan trend encourages more and more restaurants, cafeterias, and catering services to offer vegetarian and vegan options on the menu. Textured vegetable proteins can be diversified into elements in a wide variety of dishes, starting from plant-based burger patties and sausages to stir-fries and pasta dishes. It thus opens an avenue for textured vegetable protein manufacturers to collaborate with foodservice companies on new menu item innovations that will attract the growing number of consumers who aim to avoid meats. By capitalizing on this trend, growth in market share can be gained, not only in terms of sales but also for sustainable and entirely plant-based diets in the foodservice sector.

What factors contribute to granules holding the highest market share in the textured vegetable protein market?

Granules dominate the market for textured vegetable proteins due to their versatility and ease of use in a wide range of food applications. Their popularity stems from their desirable texture and high protein content, which closely mimics meat, making them a favored choice among manufacturers of meat substitutes and nutritional fortification solutions. This significant market share highlights the rising consumer demand for plant-based proteins and the accelerating pace at which producers are adopting innovative food solutions.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264440297

Asia Pacific to grow at the highest rate in the textured vegetable market during the forecast period.

The surge in Western dietary habits, combined with higher disposable incomes and a shift towards healthier and more eco-friendly food choices, is expected to drive this growth. Additionally, government initiatives focused on food security and sustainability are boosting the demand for plant-based proteins, including textured vegetable protein. The expanding population and increasing urbanization in this region also contribute to the rising demand for convenient and nutritious options like meat alternatives.

Top Textured Vegetable Protein Companies

The key players in this market include ADM (US), Roquette Frères (France), Ingredion (US), Shandong Yuxin Bio-Tech Co., Ltd. (China), DSM (Netherlands), The Scoular Company (US), Beneo (Germany), International Flavors & Fragrances, Inc. (US), Cargill, Incorporated (US), MGP (US), Gushen Biological Technology Group, Co., Ltd. (China), Axiom Foods, Inc., (US), Foodchem International Corporation (China), PURIS (US), and Dacsa Group (Spain). These market participants are emphasizing the expansion of their footprint via agreements and partnerships. They maintain a robust presence in North America, Asia Pacific, South America, RoW, and Europe, and they are supported by manufacturing facilities and well-established distribution networks spanning these regions.