The global automotive heat shield market, by value, is projected to grow at a CAGR of 7.8 % from 2015 to 2020 to reach USD 15.1 Billion by 2020. Asia-Pacific is the largest market for automotive heat shields, followed by Europe and North America. Technological advancements have made automotive heat shields safer and more effective over the past few years. The materials used in automotive heat shield fabrication include aluminum, nylon, and ceramic.

The automotive heat shield market has been further segmented by vehicle type into passenger car, light commercial vehicle, and heavy commercial vehicle. Given the growing demand for light commercial vehicles in the North American and Asia-Pacific regions, this segment of the automotive heat shield market is expected to grow rapidly, at a CAGR, by value, of 8.5% during the forecast period.

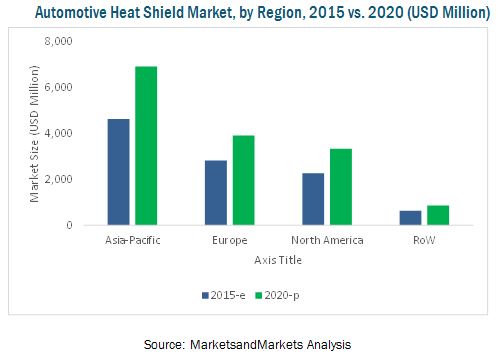

ASIA-PACIFIC: TO REMAIN A DOMINANT MARKET FROM 2015 TO 2020

The automotive industry in Asia-Pacific has witnessed year-on-year growth in terms of vehicle production volume. It is the leading producer of automobiles, and is estimated to retain its position during the forecast period. The region houses some of the fastest-developing economies in the world, including China and India. The Asia-Pacific automotive heat shield market is projected to exhibit steady growth from 2015 to 2020, with China being the largest contributor to this growth. This is mainly attributed to production expansions made by automobile manufacturers to cope with rising consumer demand for fuel-efficient vehicles. Implementing new technologies, setting up additional manufacturing plants, and creating a value-added supply chain between manufacturers and material providers have created a platform for future growth in this region.

NORTH AMERICA & EUROPE: SET TO BE POTENTIALMARKETS IN THE NEAR FUTURE

The North American automotive heat shield market is expected to grow at a higher rate than the European market. North America is a hub for several established OEMs. OEMs in the region have been focusing on developing low carbon-emission and fuel-efficient vehicles to comply with federal mandates. Several OEMs are planning to set up production facilities in Mexico and Canada, which would drive the demand for automotive heat shields in the future. Europe is also a major hub for OEMs; however, Eastern Europe still lags behind Western European countries such as the U.K., Germany, France, and Spain, in terms of technology. OEMs, therefore, have an opportunity to expand their footprint in Eastern Europe and foster demand for automotive heat shields in the region.

TURBOCHARGER HEAT SHIELD: FASTEST-GROWINGAPPLICATION SEGMENT

The turbocharger heat shield provides thermal insulation for the automotive turbocharger. It generally takes the form of coatings, wraps, or blankets. This heat shield reduces turbo lag, while serving as a heat barrier that shields and protects engine components, hoods, and painted surfaces from radiant heat. The increasing demand for fuel-efficient vehicles and the growing trend of enginedownsizing are expected to propel the demand for turbocharger heat shields in coming years.

The global automotive heat shield market is estimated to be dominated by Autoneum Holding AG (Switzerland), ElringKlinger AG (Germany), and Federal-Mogul Corporation (U.S.). These companies collectively account for a major share of the automotive heat shield market. The top players have been adopting every possible strategy to acquire new customers and to increase the demand for their products. Key strategies adopted by these players to capitalize on available opportunities include new product launches, agreements/joint ventures, and mergers & acquisitions.