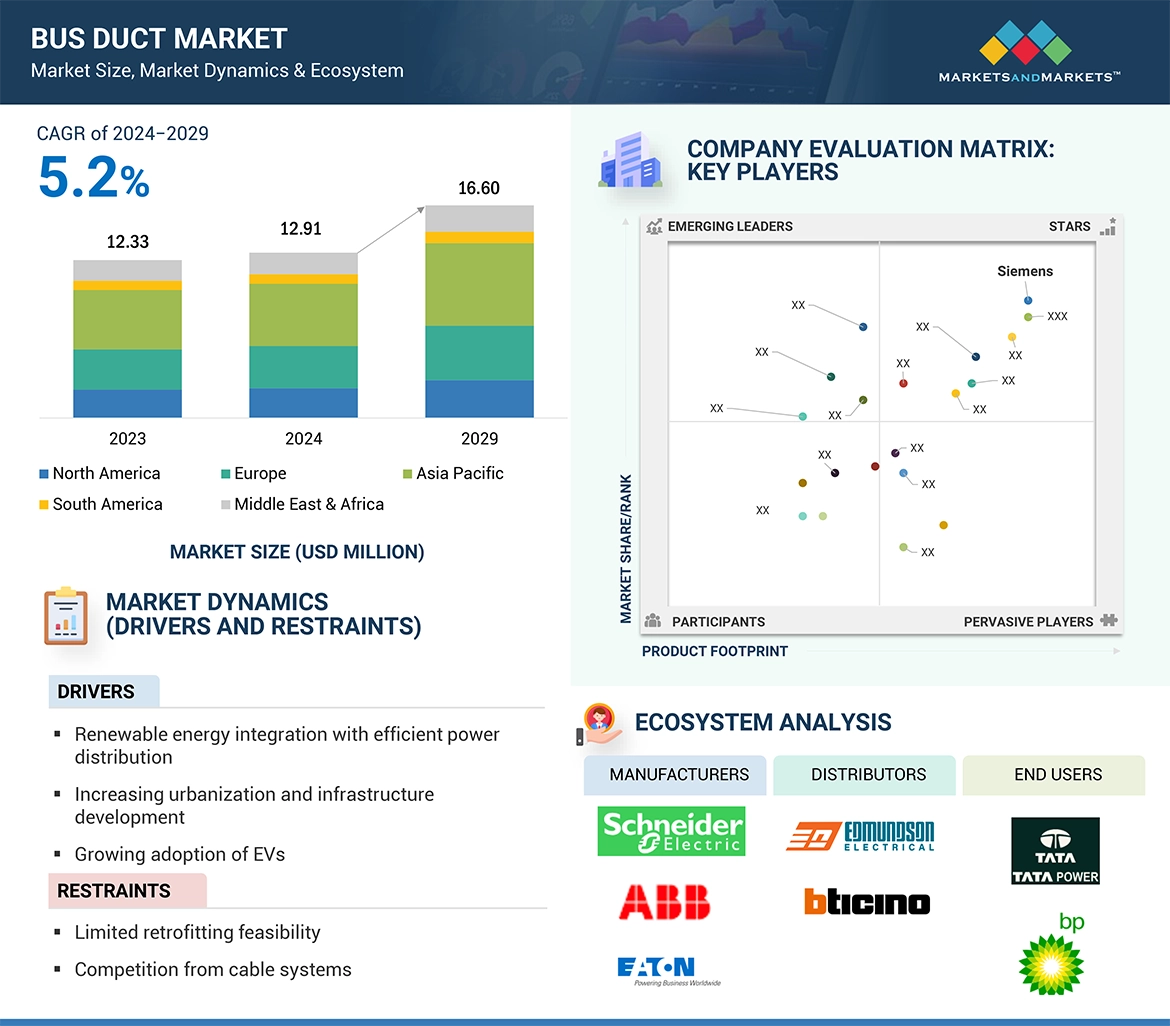

According to a research report, Bus Duct Market is also expected to increase from an estimated USD 12.91 billion in 2024 to USD 16.60 billion by 2029 at a compound annual growth rate of about 5.2% during the forecast period. It is projected to be mainly propelled by elevated electrification and infrastructure, especially in industries such as utilities and transportation, who are high in demand for efficient distribution systems. Renewed government policies that attempt to speed up a shift towards renewable power and an improved grid modernization form fuel for the growth happening in the market. The embedding of smart technologies, such as automation, digital sensors, and data analytics, inside bus duct systems has increased their performance, efficiency, and reliability. Such emerging technologies also help in reducing energy waste, decreasing material loss during production, and lowering the associated operational cost, making bus ducts not only sustainable but also cost-effective. All these are expected to propel further growth in the bus duct market and make it an integral component of the ongoing industrial modernization and energy transition.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14743619

Data Centers, by end-user segment

The data center segment is expected to be the fastest-growing market for bus ducts during the forecast period, due to the rapid global expansion of cloud computing, artificial intelligence, big data analytics, and the Internet of Things, which are driving unprecedented demand for data storage and processing capabilities. For any modern data center, their operations are very energy intensive and require power distribution systems that are efficient, reliable, and scalable. Hence, bus ducts, providing such attributes, are now widely preferred. Bus ducts tend to have less energy losses in power distribution, higher heat dissipation, and easier installations when compared to traditional cabling systems. In addition, the increased investment in hyperscale data centers and edge computing facilities across the North American, Asia Pacific, and European regions is also driving the growth. The demand for sustainability and green data centers is another vital factor as bus ducts support energy efficiency and have reduced environmental footprints. The government as well as private investments on the part of digital infrastructures push the data center segment on the growth ladder and act as a critical driving factor for the bus duct market.

Copper, by material

The copper segment will be the largest market by material in the bus duct market during the forecast period. This is due to superior electrical and thermal conductivity, making copper the preferred material for power distribution applications. Copper bus ducts have low electrical resistance, which means energy loss is at a minimum and efficiency is increased. It offers reliable performance in demanding environments, such as industrial facilities, utilities, and power generation plants, due to its high durability and mechanical strength. Additionally, copper has excellent corrosion resistance and thermal and electrical stress capabilities, which make it a good choice for high-current applications, especially in utilities and renewable energy installations. Advances in copper processing technologies, such as flexible and laminated bus ducts, have added to its performance, offering compact, space-saving designs with improved reliability. Moreover, growth in green building initiatives, along with increasing renewable energy projects, are driving the market for copper bus ducts, as these align with the sustainability objective of minimizing energy loss while maximizing efficiency. All these factors together contribute to the growth of the copper segment in the bus duct market.

Regional Analysis

Asia Pacific is expected to hold the biggest market share in bus ducts throughout the forecast period for several significant growth drivers that are set in motion. The speed at which these countries of emerging economies- China, India, and Southeast Asia undergo industrialization and urbanization raises the bar in terms of demand for more efficient power distribution systems. The need for efficient and scalable electrical distribution solutions, such as bus ducts, is growing as more infrastructure projects like smart cities, commercial buildings, and industrial facilities are coming up. In addition, the regional focus on renewable energy adoption and electrification of transportation, especially in electric vehicles (EVs), is further adding momentum to the need for advanced power distribution systems. Asia Pacific’s thrust for sustainable development and energy-efficient solutions goes hand in hand with the demand for eco-friendly and energy-saving bus duct technologies. In addition, increasing investments in data centers and smart grid technologies further support the region’s dominance. Asia Pacific is to continue its dominance in the bus duct market in the following years, driven by potential growth in infrastructure development and adoption of renewable energy, which is also growing at an industrialization rate.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=14743619

Key Players

Some of the major players across the globe in this bus duct market are ABB (Switzerland), Siemens (Germany), Schneider Electric (France), Eaton (Ireland), and Legrand (France). These companies have aggressively embraced various strategies to enhance their presence and respond to the increasing demand for efficient power distribution systems. Key strategic steps include the development of new products for advanced bus duct technology, a strategic acquisition that broadens the present product offerings, and partnerships that expand their reach into newer markets.