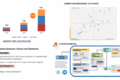

The Future of EV manufacturing is projected to grow from 15.7 million units in 2024 to 46.3 million units by 2035, at a CAGR of 10.3%.

OEMs confront major obstacles in the areas of scalability, time to market, technological integration, and—above all—capital investment as sales of electric vehicles continue to climb. Plant and platform sharing across other OEMs, manufacturing plant layout, and automation technologies continue to be major challenges and areas of focus, even though EV technology is helping to some extent with the capital investment challenge.

Advances in flexible and modular assembly structures, which enable automakers to construct several models on shared platforms like skateboard architecture, are driving the future of electric car manufacturing. This strategy shortens time to market, increases scalability, and lowers production costs. Production efficiency and quality control are further optimized by advancements in automation, digital twins, and artificial intelligence manufacturing systems. Furthermore, in order to reduce the carbon footprint, sustainability goals are changing the manufacturing landscape by placing more of a focus on circular economy principles, localized supply chains, and equipment driven by renewable energy. All of these elements work together to make EV production a flexible and dynamic sector that can fulfill rising consumer demand while overcoming environmental and technological obstacles.

Over the course of the forecast period, commercial vehicles will expand at the greatest CAGR.

The market for commercial vehicles is anticipated to develop at the quickest rate in the electric vehicle sector due to rising demand for environmentally friendly transportation options, stricter pollution standards, and advancements in battery technologies that lower costs and enhance range. In order to meet these demands, solve urban air quality concerns, and lower operating costs for fleet operators, OEMs including Volvo, Daimler Truck AG, and Ford Motors are concentrating on the development of electric commercial vehicles, including trucks, buses, and vans. For example, Ford stated in August 2024 that it would begin producing electric vehicles in 2026 with a commercial van that would be put together at its Ohio Assembly Plant. Additionally, governments everywhere are aiding this shift through infrastructure investments, incentives, and subsidies, such growing commercial-scale charging networks. In order to develop competitive, future-ready EV portfolios, OEMs are embracing these opportunities by introducing novel models, establishing strategic alliances, and incorporating cutting-edge technologies like telematics and autonomous driving systems. This change places the commercial vehicle category as a major driver in the growth trajectory of the EV industry and enhances their market presence while also being in line with global sustainability aspirations.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=255751150

OEMs’ efforts to implement a circular economy strategy propel market expansion.

OEMs’ transition to a circular economy strategy, which places a strong emphasis on sustainability and resource efficiency, is influencing the direction of the EV manufacturing industry. Manufacturers are using strategies such as recycling battery components, repurposing production waste, and designing automobiles to facilitate material recovery and disassembly. BMW of North America and Redwood Materials, for example, announced in September 2024 that they would recycle lithium-ion batteries from all electric, plug-in hybrid-electric, and mild hybrid vehicles made by BMW, MINI, Rolls-Royce, and BMW Motorrad in the United States. The collaboration is the next phase in developing a closed-loop circular value chain for lithium-ion batteries in the United States and shows a common dedication to sustainability. Long-term growth in the EV market is fueled by OEMs’ integration of circular principles, which also improves their competitiveness and aligns with customer desire for eco-friendly solutions and worldwide regulatory challenges.

Throughout the forecast period, Asia Pacific (excluding China) will expand at the greatest CAGR.

Due to encouraging government regulations, rising infrastructure investment, and rising consumer awareness of sustainability, Asia Pacific (excluding China) is expected to become the market with the fastest rate of growth for electric vehicles. For example, in an effort to fortify its battery supply chain, Japan will provide further subsidies for the development of batteries for electric vehicles, promising up to USD 2.4 billion in support for associated initiatives by Toyota Motor and other significant corporations. The development of electric vehicles is being actively encouraged by nations like South Korea, Japan, and India. Mahindra & Mahindra and Tata Motors are expanding their operations in India with affordable electric vehicles and indigenous supply networks. Using cutting-edge battery technologies, Toyota and Honda of Japan are concentrating on hybrid and all-electric platforms. Hyundai and Kia of South Korea are making significant investments in EV platforms like E-GMP in an effort to become the world’s leading EV manufacturers. By 2030, the Hyundai Motor Group intends to invest USD 16 billion in electrification. In addition to local efforts to assist the production and assembly of EV components, Indonesia and Thailand are establishing themselves as regional EV centers, drawing investment from international companies like BYD and Hyundai. The Rayong factory, located south of Bangkok, would employ about 10,000 people and have an annual production capacity of 150,000 vehicles according to BYD’s USD 486 million investment. To hasten the shift to electric vehicles, these initiatives are bolstered by aggressive government goals, green mobility subsidies, and public-private partnerships.

In order to ensure compliance, innovation, quality, supply chain efficiency, and market readiness, a variety of stakeholders are involved in the EV manufacturing ecosystem, including OEMs, EV assembly lines, Tier-2 and Tier-1 component manufacturers, raw material suppliers, certification providers, EV design service providers, and equipment and technology providers. Among the major OEMs are General Motors, BYD, Tesla, and Volkswagen. Among the major producers of Tier I components are CATL, Continental, Bosch, LG Solution, and others. Siemens AG, ABB, Rockwell Automation, and others are industry leaders in EV plant automation.

Key Market Players

Major players operating in the Future of EV Manufacturing market are Tesla (US), BYD (China), Volkswagen (Germany), SAIC Motor (China), Stellantis NV (Netherlands) and among others.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=255751150