The embolotherapy market is witnessing a loss of business, and the trend is expected to continue till December 2020. Unfavorable changes in regulations and guidelines are hampering the growth of this industry. Major regulatory authorities across the globe (such as CDC, WHO, MHRA, TGA, and EMA) have identified that cancer patients are at greater risk of COVID-19 infection than healthy adults.

Globally, there were over 840,000 new cases diagnosed in 2018. (Source: World Cancer Research Fund). Furthermore, over the last decade, kidney cancer incidence rates increased by 42% in the UK. In females, the incidence rates increased by 44%, while there was a 38% incidence rate in males. (Source: Cancer Research UK).

The high success rate and less post-operative complication rate associated with embolotherapy procedures coupled with the rising incidences of liver cancer and hepatocellular cancer will further boost the demand for embolotherapy devices in the near future. Liver cancer is fifth-most-common cancer in men and the ninth-most-common in women.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=185897830

Healthcare markets are witnessing a dearth of well-trained surgeons (including neurosurgeons and radiologists). The Association of American Medical Colleges (US) has estimated a deficit of 41,000 general surgeons in the US by 2025 (Source: Association of American Medical Colleges US, 2017).

Similarly, India is also facing an acute shortage of oncologists, radiotherapists, and surgical oncologists. With 1.8 million cancer patients in the country, there is only one oncologist to treat every 2,000 patients. The shortage of oncologists and radiologists in several countries worldwide is expected to affect the adoption of embolotherapy procedures.

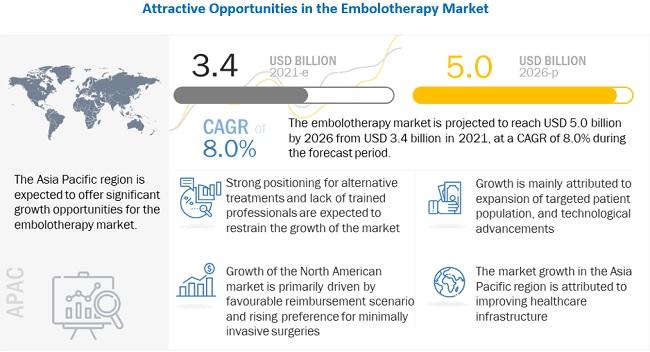

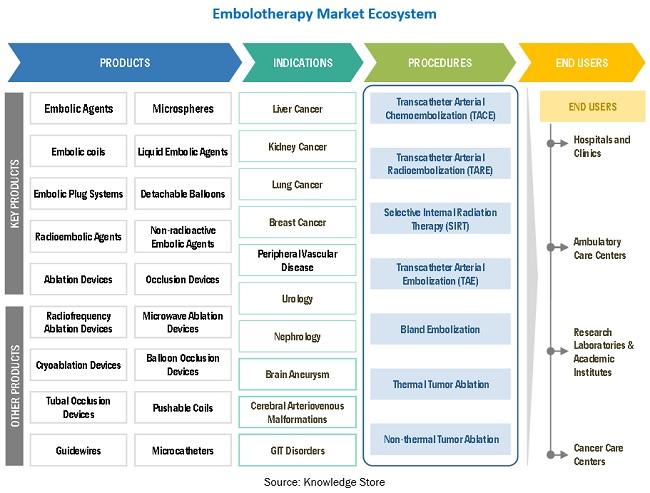

In terms of application, embolotherapy is classified into cancer, peripheral vascular diseases, neurological diseases, urological & nephrological disorders, and gastrointestinal disorders. The cancer segment commanded the largest share of the market in 2020, and the same segment will grow at the highest CAGR over the forecast period between 2021 and 2026.

Hospitals and clinics are the key end users of embolotherapy devices. This segment covers the market for embolotherapy devices used in big hospitals, small clinics, and critical care units.

The growing adoption of minimally invasive surgical procedures (including vascular, urological, and neurological), increasing purchasing power of major healthcare providers across developed countries (owing to the consolidation of healthcare providers), and the greater availability of reimbursements for target procedures in the US and major European countries are the major factors that are expected to drive the demand for embolization devices in hospitals and clinics.

The major players in the embolotherapy market are Boston Medical Corporation (US), Terumo Medical Systems (Japan), Medtronic (US), Johnson & Johnson (US), and Stryker Corporation (US). Other key players in the embolization therapy market include Sirtex Medical Limited (US), Abbott Laboratories (US), Acandis GmbH (Germany), Balt (France), Cook Medical (US), Kaneka Corporation (Japan), Penumbra, Inc. (US).