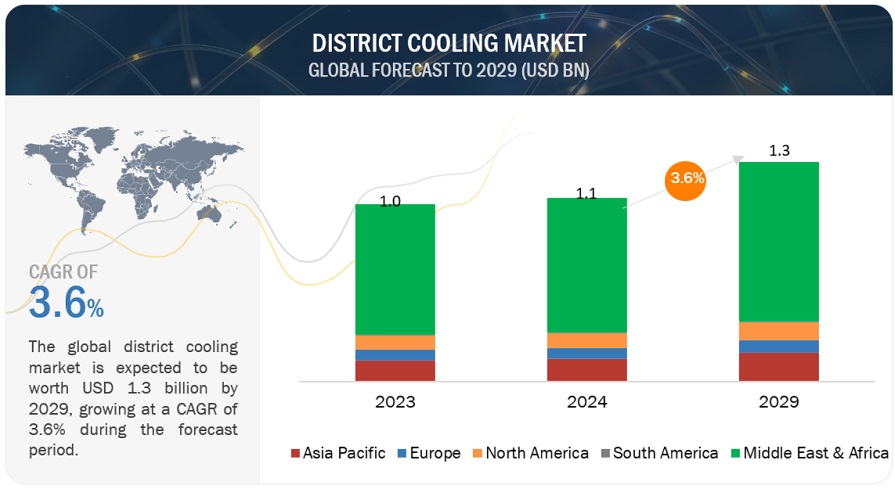

The global District Cooling Market in terms of revenue was estimated to be worth $1.1 billion in 2024 and is poised to reach $1.3 billion by 2029, growing at a CAGR of 3.6% from 2024 to 2029 according to a new report by MarketsandMarkets™.

Commercial, Industrial, and Residential are the major applications of district cooling. The District Cooling Market is majorly concentrated in Middle East & Africa.

Energy efficiency improvement is a key driver for the district cooling market, due to its potential for substantial energy savings and environmental benefits. District cooling systems are designed to optimize the use of energy by centralizing cooling production, which reduces the overall energy consumption compared to individual cooling units. This centralization allows for the use of advanced, energy-efficient technologies that are not feasible on a smaller scale. As energy costs rise and environmental concerns grow, businesses and municipalities are increasingly seeking solutions that lower their energy usage and carbon footprint. Additionally, many governments offer incentives and support for adopting energy-efficient systems, further driving the demand for district cooling. This focus on energy efficiency helps organizations achieve sustainability goals while also improving their bottom line, making it a crucial factor in the market’s growth.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=27186936

Electric chillers is expected to hold largest share of the District Cooling Market in production technique segment during the forecasted period.

Electric chillers segment by production technique hold the largest share of the District Cooling Market due to their high efficiency, reliability, and widespread availability. They can be easily integrated into existing infrastructure and are capable of producing large amounts of chilled water needed for district cooling systems. Additionally, electric chillers benefit from advancements in technology, which have significantly improved their energy efficiency and reduced operational costs. This makes them an attractive option for developers and operators seeking to minimize environmental impact and comply with increasingly stringent energy regulations. Their versatility in handling varying cooling loads across different applications further solidifies their dominant market position.

Commercial application segment accounted largest share of the global district cooling market

The commercial segment holds the largest share of the District Cooling Market because commercial buildings have high and continuous cooling demands. District cooling systems provide an efficient, reliable, and cost-effective solution to meet these needs, reducing energy consumption and operational costs. Additionally, increasing energy efficiency regulations and sustainability goals in the commercial sector make district cooling an attractive and scalable option.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=27186936

Asia Pacific is expected to be the fastest-growing region of the global District Cooling Market.

The surge in construction activities, alongside a burgeoning population and evolving climatic conditions, are critical drivers of this regional market growth. Additionally, the push towards sustainable and energy-efficient cooling solutions in urban developments, increased investments in infrastructure, and government initiatives promoting eco-friendly technologies are further catalyzing the market. The integration of advanced technologies and innovations in district cooling systems is also anticipated to enhance operational efficiency and reduce energy consumption, thereby contributing to the market’s expansion in the coming years.

Key Players

Some of the major Key Players in the global District Cooling Market are Johnson Controls Inc. (US), Daikin Industries, Ltd. (Japan), Trane Technologies plc (Ireland), Mitsubishi Heavy Industries, Ltd. (Japan), Danfoss A/S (Denmark), Shinryo Corporation (Japan), LOGSTOR Denmark Holding ApS (Denmark), Emirates Central Cooling Systems Corporation PJSC (UAE), Tabreed (UAE), Emicool (UAE).