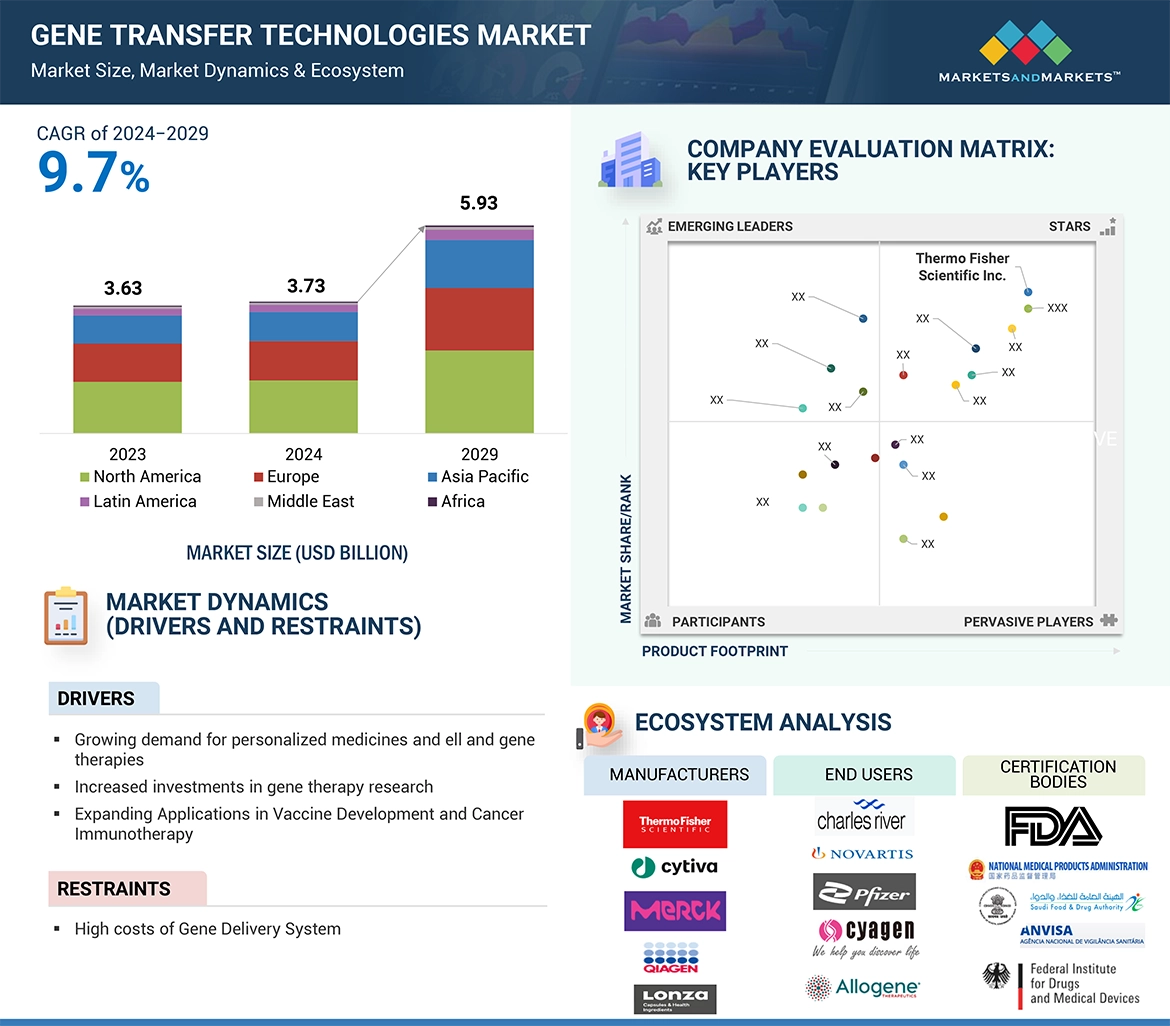

The global gene transfer technologies market, valued at US$3.63 billion in 2023, is forecasted to grow at a robust CAGR of 9.7%, reaching US$3.73 billion in 2024 and an impressive US$5.93 billion by 2029. The increasing usage in vaccine development and applications in cancer immunotherapy; is one of the major factors driving the growth of the gene transfer technologies market. Additionally, growing need for personalized medicines and investments in gene therapy research. The presence of key market players in the North American region and the strong emphasis on adopting cell & gene-based therapies is accelerating the growth of the market.

Browse in-depth TOC on “Gene Transfer Technologies Market”

771 – Tables

56 – Figures

524 – Pages

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=74062902

DRIVER: growing demand for personalized medicine and cell & gene therapies

Personalized medicine has been at the heart of the health care industry’s research, which provides drug treatments according to the patient’s profile, with significantly higher outcomes and savings. This is most obviously seen in cancer treatment therapies such as CAR-T. In CAR-T, the viral vectors engineer the T-cells specifically to target and destroy cancer cells. One such revolution is the growing role of precision and personalized medicine in the treatment of cancer and especially by developing tailored therapies from individual genetic and omics data to ensure efficacy for particular kinds of subtypes of cancers. For non-small-cell lung cancers, for instance, the detection of ALK mutations has resulted in the identification of drugs such as crizotinib. Companion diagnostics such as Myriad’s BRACAnalysis detect mutations to match patients with appropriate treatment suited to their genetic profile, leading to a better effectiveness in treatment and benefits to the patients. Similarly, the advancement further accelerated by the Precision Medicine Initiative and support from the FDA. There has been an increasingly adopted cell & gene therapy as a stand-alone treatment and, more importantly, in combination with personalized treatment.

RESTRAINT: High cost of gene transfer systems.

Development of gene transfer systems involves high capital costs, plus there is also adoption and availability. There is also a development cost, in that developing these systems requires advanced genetic engineering, including building replication-deficient adenoviruses for vaccine production. Mass production is also certainly not cheap, requiring special facilities and equipment for very high purity and potency. Technologies such as NanoSight and Zetasizer Ultra by Malvern Panalytical add an extra cost in terms of ensuring the accurate measurement and stability of viral particles.

The high expense of the gene transfer systems largely dictates the cost of the gene therapies, which also affects their access and reduces their commercial feasibility. A rare genetic disorder treated by gene therapy, for example, the spinal muscular atrophy, may be as high as USD 2 million per patient and would heavily limit access and burden the healthcare systems and insurance providers financially.

Similarly, though the CAR-T cell therapy has potential in treating specific cancers, the cost may run into over USD 373,000 per patient. This may create a hurdle in its proper adoption as well as reimbursement. A huge upfront investment, especially in developing and manufacturing and regulatory compliance, makes it expensive as well as adds to the financial hindrances. High costs of gene transfer systems add to the high cost of gene therapy. Thus, it acts as a growth barrier to the gene transfer market.

OPPORTUNITY: Rising advancement in gene editing technologies and nanotechnology

Gene editing breakthroughs, particularly the CRISPR-Cas9 system, have hugely transformed genetic research and therapies with the capability of putting targeted and precise mutations in DNA. Precision to this extent is, in fact, the aim of gene therapies as well as personalized medicine-and indeed a venue for such applications as treatments for genetic disorders like sickle cell anemia and muscular dystrophy. While with the advent of more accurate and less off-targeting second-generation CRISPR technologies, safer and more successful treatments would be provided thus propelling market growth even further. In vivo gene editing has made a lot of strides over the more established ex vivo method, so it may be faster and cheaper to directly change the genes in tissues, but delivery methods including Cas9 still present problems in terms of efficiency and safety.

Of these, some of the most recent developments include improved smaller Cas proteins and better nanocarriers, which have heard such technical challenges related to encapsulation, safety, and targeting. Others are attempting to minimize such off-target effects by using tissue-specific promoters or constructing the nanoparticles with spatiotemporal control and ligand-mediated targeting.

Nanotechnology also revolutionizes the methods of gene transfer . Engineered nanoparticles, namely liposomes and polymeric nanoparticles, can deliver genetic material in a more targeted and precise manner with therapy enhancement and reduced toxicity. For instance, mRNA vaccines developed by Pfizer-BioNTech and Moderna utilize lipid-based nanoparticles to deliver genetic instructions which will stimulate immunity against COVID-19. These advancements thereby create opportunities for greater application of nanotechnology in the gene transfer systems.

The application of advanced gene editing, nanotechnology, in integrating these into gene transfer systems, increases their capabilities, efficiency, and targeting. All these drives the gene transfer market as the ability to formulate innovative therapies and personalized treatments tends to open new avenues toward addressing complex medical conditions that result in a better outcome in patients.

CHALLENGES: Scalability of production

Manufacturing of viral vectors, like that of AAV and lentivirus, involves complex processes such as cell culture and purification requiring resource-intensive and expensive scaling up. The efficiency of analytics would be a basis of the potent, pure, stable, and identified status of AAV products for the maintenance of product safety and efficacy in clinical applications. However, current analytical methods designed for smaller biologics were primarily made for and, thus, presented a considerable number of challenges when applied to AAVS. Such challenges entail a large molecular weight by AAVS, oligomeric complexity, and low concentrations of viral particles in comparison to traditional biologics such as mAbs. For example, the level of empty to full capsid is an important CQA for AAV manufacturing because empty viral particles do not contain therapeutic genomes, but they can induce immune responses or generally affect therapeutic effects. The current methodologies of analytics tend to be less accurate, slow, and inapplicable to real-time monitoring. One major need is the development of stronger methods with higher throughput, greater sensitivity, and dynamic range than typical AAV titers. Gene therapies also often call for site-specific, disease-or population-specific vectors that can’t be standardized across many diseases or patient populations. Consequently, mass production is challenging. Even at commercial scale, there are stiff conditions related to safety, quality, and consistency, making things even more difficult and costly to produce. That’s why some therapies like Zolgensma cost millions per dose; it would be severely challenging to manufacture such therapy at a lower cost. Companies like ElevateBio (US) and Oxford Biomedica (UK) are looking to Al-driven platforms to accelerate operations, and companies like Catalent and Lonza, who are among the top CDMOs, are scaling their production capacity more efficiently through collaborations with several firms.

Request Sample Pages : https://www.marketsandmarkets.com/requestsampleNew.asp?id=74062902

Product segment dominated the gene transfer technologies market in 2023.

The product segment is segmented into instruments, consumables, reagents, kits & assays, and other products. The reagents, kits & assays gene transfer technologies segment dominated product segments owing to various factors such as increasing adoption of gene therapies and cell therapies across pharmaceutical and biotech research. The consumables segment is anticipated to grow at a significant CAGR owing to increase in the activities for research and development in genetic engineering is rising the demand for good quality laboratory materials. The product segment is segmented into instruments, consumables, reagents, kits & assays, and other products. Factors such as increasing adoption of gene therapies and cell therapies across pharmaceutical and biotech research contribute in the market growth.

Viral Vector segment dominated the gene transfer technologies market in 2023.

The gene transfer technologies market is segmented by mode into viral and non-viral vector. The viral segment dominated the market in 2023. The segment’s dominance is attributable to increasing technological developments for cell-based therapies, innovation in viral vector manufacturing including automation and scalable production technique. Increased use of Adeno-associated viruses (AAV), lentiviruses, and retroviruses for various therapeutic applications coupled with increased investment by key market players in the advancement of viral vector technology is further likely to boost the segmental growth in coming years.

In vivo segment dominated the gene transfer technologies market in 2023.

Based on the method, the market is divided into ex vivo, in vivo and in vitro. The in vivo method dominated the market in 2023. The main driver for the growth of in vivo segment include advancement in vector technologies particularly viral vectors like adeno-associated viruses (AAVs) and lipid nanoparticle (LNP) system, increased prevalence of genetic disorders and chronic diseases that could heighten demand for innovative therapeutic solutions and expanding application of LNPs in mRNA vaccines. Increased investment from pharmaceutical companies and government initiatives, alongside regulatory support for innovative gene therapies is also significantly supporting the growth of segment.

Therapeutic application segment dominated the gene transfer technologies market in 2023.

The application segment is segmented into research, therapeutics, and other applications. The therapeutics application segment dominated application segment in 2023. An increased investment in gene therapies, rising chronic diseases, and need for new approaches in treating these diseases, as well as the advancement of delivery methods which enhance efficacy and safety are supposed to contribute to the growth of this market.

The end user segment is likely to grow at a significant CAGR from 2024 to 2029.

The end-user market is categorized into the pharmaceutical & biotechnology companies, academic & research institutes and other end users. The pharmaceutical & biotechnology companies dominated the segment in 2023; the academic & research institutes are likely to grow at a significant CAGR. Advancement in the discovery of new gene therapies addressing rare genetic disorders, cancers, and chronic diseases and development in gene editing technologies include CRISPR and zinc finger nucleases drive growth in the segment. Apart from this, favourable regulatory support and strategic partnerships with biotech companies further boost prospects for growth.

Recent Developments of Gene Transfer Technologies Market

- In September 2024, Cytiva launched the RNA delivery LNP kit designed for use with the NanoAssembl Ignite and Ignite+ systems, extending the GenVox-ILM product line to accelerate mRNA and siRNA vaccine development.

- In March 2024, Sartorius launched RPLUS, AAV-RC2, a Bercar plasmid for adeno-associated virus vector 2 (AAV2) production, further expanding the plasmid portfolio to address the range of AAV serotypes.

- In September 2024, MaxCyte and Kamau Therapeutic entered into a strategic platform license (SPL) agreement under which Kamau obtained non- exclusive research, clinical, and commercial rights to utilize MaxCyte’s Flow Electroporation technology and EXPERT platform to support its homology-directed repair (HDR) novel gene correction technology.

- In August 2024, Merck acquired Mirus Bio to advance Merck’s integrated offering for viral vector manufacturing

Content Source:

https://www.marketsandmarkets.com/Market-Reports/gene-transfer-technologies-market-74062902.html

https://www.marketsandmarkets.com/PressReleases/gene-transfer-technologies.asp