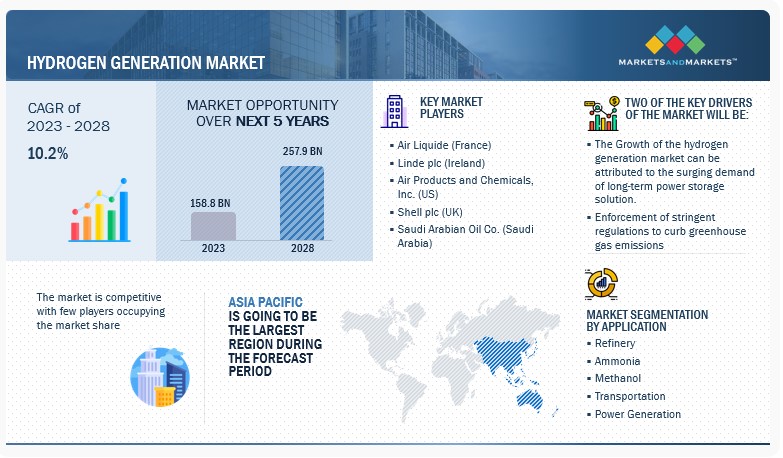

According to a research report “Hydrogen Generation Market by Technology (SMR, ATR, POX, Coal Gasification, Electrolysis), Application (Refinery, Ammonia, Methanol, Transportation, Power Generation), Source (Blue, Green, Gray), Generation Mode Region – Global Forecast to 2028″ published by MarketsandMarkets, the global hydrogen generation market is projected to reach USD 257.9 billion by 2028 from an estimated USD 158.8 billion in 2023, at a CAGR of 10.2% during the forecast period. The growing demand for cleaner fuels is one of the major factors driving the hydrogen generations market. Global hydrogen generation demand has been increasing gradually due to goals set to achieve net zero emissions in recent years. Hydrogen has long been recognized as a possible low-carbon transportation fuel, but incorporating it into the mix of transportation fuels has been a challenge. It has an advantage over fossil fuels and is becoming expensive day by day. There has been enormous demand for hydrogen for use in fuel-cell electric vehicles and rockets in the aerospace industry. In the transportation sector, fuel cell costs and refueling stations determine how competitive hydrogen fuel cell automobiles are, but lowering the supplied price of hydrogen is a top concern for truck manufacturers. There are a few low-carbon fuel options for ships and aircraft, providing an opportunity for developers of hydrogen-based fuels. Hydrogen fuel cells are widely used in lightweight vehicles, such as bicycles, cars, buses, trains, material handling equipment, boats, ships, commercial aircraft, auxiliary power units (APUs) of aircraft, marine vessels, and specialty vehicles. However, the risks associated with high initial investment for setting up hydrogen production plants and technological challenges in implementing hydrogen to natural gas networks have hindered the growth of the market in recent years and are expected to restrain the market’s growth during the forecast period.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=494

The Grey Hydrogen, by source, is expected to be the largest segment during the forecast period.

Based on source, the hydrogen generation market has been split into Blue hydrogen, Grey hydrogen and Green hydrogen. The hydrogen generation market for grey hydrogen is anticipated to have the biggest market share over the forecast period. Due to its extensive history of production, use, and versatility, grey hydrogen is frequently more in demand. Additionally, green Hydrogen is the fastest growing segment in the forecast period. Green hydrogen is produced without emitting greenhouse gases, making it a crucial tool for decarbonizing various sectors of the economy, such as transportation, industry, and heating.

The transportation segment, by application, is expected to grow at the highest CAGR during the forecast period.

This report segments the hydrogen generation market based on application into six segments: petroleum refinery, ammonia production, methanol production, transportation, power generation and others. The transportation segment is expected to grow at the highest CAGR during the forecasted period, owing to the extensive decarbonization efforts in the road, marine and aviation sector in North America, Europe, and Asia Pacific. As a clean and efficient energy carrier, hydrogen is increasingly being employed in a variety of transportation applications. Hydrogen is being explored as a potential alternative for heavy-duty trucks such as delivery trucks and long-haul freight vehicles and also utilized in maritime applications.

Asia Pacific is expected to be the fastest-growing region in the hydrogen generation market.

Asia Pacific is expected to be the fastest growing region in the hydrogen generation market during the forecast period. The Asia Pacific region comprises major economies such as China, Japan, India, Australia, and South Korea. The hydrogen generation market in Asia Pacific is primarily fueled by the increasing number of petroleum refineries and usage of hydrogen in these refineries. Asia Pacific is one of the leading markets for adopting green technologies to meet the government targets for reducing GHG emissions. Japan and South Korea have been heavily investing in fuel cell adoption since 2009 because of the commercial deployment of Japanese fuel cell micro-CHP products. Japan is the first nation to commercialize fuel cells and is supporting projects related to the use of fuel cells in residential and automotive applications. It aims to deploy green hydrogen on a large scale. The country plans to have 200,00 green hydrogen fuel cell vehicles and 320 hydrogen refueling stations by 2025 to meet the global carbon emission standards.

Ask Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=494

Key Market Players

Some of the major players in the hydrogen generation market are Air Liquide (France), Linde plc (Ireland), Air Products and Chemicals, Inc. (US), Shell plc (UK), and Saudi Arabian Oil Co. (Saudi Arabia). The major strategies adopted by these players include new product launches, acquisitions, contracts, agreements, partnerships, joint ventures, collaborations, investments, and expansions.