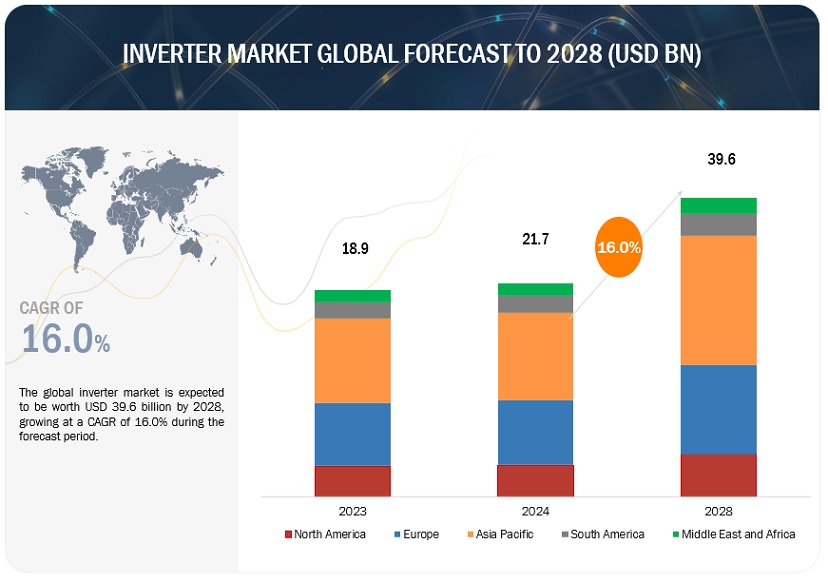

According to a research report “Inverter Market by Type (Solar Inverters, Vehicle Inverter), Output Power Rating (Upto 10 kW, 10-50 kW, 51-100 kW, above 100 kW), End User (PV Plants, Residential, Automotive), Connection, Voltage, Sales Channel & Region – Global Forecast to 2028″ published by MarketsandMarkets, the Inverter market is projected to reach USD 39.6 billion by 2028 from USD 18.9 billion in 2023, at a CAGR of 16.0% during the forecast period.

The simplicity of installation for both string and micro inverters is the main factor propelling the global market’s expansion. The industry has grown as a result of increased investment in the development of renewable power infrastructure and the rise in demand for electricity from diverse uses. It is projected that the renewable energy and rural electrification sectors would see a sharp increase in investment, which will present profitable prospects for industry participants. The business is growing globally as a result of the increased use of big-sized string inverters in the utility system and other commercial and industrial sectors. These inverters make it easier to install huge solar systems since they can link many solar panels.

Download PDF Brochure – https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=263171818

Above 500 V, by output voltage, is expected to be the second fastest growing segment during the forecast period.

Based on output voltage, the Inverter market has been split into 100-300 V, 300-500 V, and above 500. The above 500 V is expanding mostly as a result of its use in utility-scale renewable energy projects and large-scale industrial applications. For the purpose of converting and controlling the significant power outputs of wind and solar farms, these high-voltage inverters are essential. The global adoption of large-scale renewable energy programmes and high-capacity industrial operations is driving up demand for inverters that operate above 500V. The expansion of this market is a result of the worldwide trend towards large-scale clean energy production and the requirement for strong, high-capacity inverters to enable these powerful and far-reaching applications.

The above 100 kw segment, by output power rating segment, is expected to be the fastest segment during the forecast period.

This report segments the Inverter market based on output power rating into below 10 kw, 10-50 kw, 50-100 kw, and above 100 kw . The above 100 kW output power rating segment in the inverter market is growing due to the escalating demand for high-capacity inverters in large-scale industrial and commercial applications. Industries and enterprises increasingly seek powerful inverters to handle substantial energy loads efficiently. This trend aligns with the expanding adoption of renewable energy solutions, where solar and wind projects demand inverters with capacities exceeding 100 kW to accommodate higher power outputs. As industries prioritize sustainable practices, the growth in this segment reflects the need for robust, high-power inverters to support large-scale clean energy initiatives.

North America is expected to be the second largest region in the Inverter market

Considering many of factors, North America is the second-largest region in the inverter industry. An expanding market for renewable energy, especially in the US and Canada, drives up demand for inverters for solar and wind power systems. The market for inverters is growing as a result of supportive government policies and incentives that encourage the use of renewable energy. Increased inverter deployment is also a result of the region’s concentration on grid upgrading and the electrification of numerous sectors. Furthermore, the need for inverters is being driven by a shift towards clean energy and a greater awareness of sustainability, which is why North America is a major player in the worldwide inverter market.

Speak to Analyst – https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=263171818

Some of the major players in the Inverter market are Huawei Technologies Co., Ltd. (China), SUNGROW (China), SMA Solar Technology AG (Germany), Power Electronics S.L. (Spain), and Fimer Group (Italy).The major strategies adopted by these players include sales contracts and agreements.