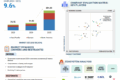

The global Software Defined Vehicle market size is projected to grow from USD 213.5 billion in 2024 to USD 1,237.6 billion by 2030, at a CAGR of 34.0%. The growth of demand for SDVs in the global market is influenced by various factors such as an increasing demand for consumer engagement, receiving continual over-the-air updates which guarantees that vehicle’s software is always up to date with the newest features and vehicle security improvements. These continual software upgrades can often resolve the issues remotely, leading to the reduced the recall costs, which allows OEMs to generate profit. Furthermore, new business models employed for SDVs allow real-time car diagnostics and problem solving, which improves the maintenance process.

SDV segment is expected to have significant growth opportunities in global Software Defined Vehicle market.

During the forecast period, SDVs are expected to have largest growth prospects. Unlike traditional ICE vehicles, which mostly rely on predefined hardware configurations, SDVs are more flexible and adaptive in nature which allows their functionality and features to be upgraded and improved over time through continual software upgrades. Among contemporary OEMS, Tesla leveraging the first mover’s advantage and has been setting the standard for the shift toward SDVs since 2012. Legacy OEMs such as Stellantis, BMW, Volkswagen among others are currently in the transition phase, planning to move from Semi-SDVs to SDVs fully by 2030, which includes increased flexibility and agility through OTA updates that enable quick response to market demands and problem solving without requiring physical recalls. This will reduce the production and recall costs by focusing on standardizing hardware and software differentiation. Further, it prolongs the life of automobiles by upholding software upgrades.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=187205966

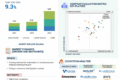

“China to lead the Software Defined Vehicle market in Asia Pacific.”

China is the largest vehicle market in the Asia Pacific and one of the biggest automobile markets worldwide, is expected to have significant growth in the Software Defined Vehicle market. China is leading the SDV market by planning to shift from SDVs to immersive SDVs with models such as JiYue 01/07, Xiaomi SU7, and NIO ET9, with features such as advanced in-vehicle workspaces with AR/VR for productivity, lifestyle synchronization with in-vehicle experiences linked to schedules and smart devices, and immersive entertainment ecosystems with multisensory features like haptic feedback and spatial audio. This transition will be led by continuous R&D and advancement in the autonomous driving technology by local software mobility providers and sophisticated automotive ecosystems integrating cloud-native technologies. Leading OEMs and technology providers in the country are utilizing open-source platforms to develop next-generation vehicle equipped with software stacks, which enhances SDV capabilities such as driving assistance, connectivity, and digitalization. SDV providers such as NIO, Li Auto Inc., ZEEKR, XPENG Inc. among others currently provide SDVs in China. Also, these SDV providers are partnering with software mobility providers to enhance their SDV capabilities. For instance, in June 2024, XPENG INC. partnered with NVIDIA Corporation for the adoption of the NVIDIA DRIVE Thor platform for its next-generation EVs. This platform will power XPENG’s XNGP AI-assisted driving system, enhancing intelligent driving capabilities. XPENG launched the G6 Coupe SUV, G9 SUV, and P7 Sedan equipped with NVIDIA DRIVE Orin, which boasts continuously upgraded AI capabilities through over-the-air updates.

Key Market Players

The Software Defined Vehicle market is dominated by global players such as Tesla (US), NIO (China), Li Auto Inc. (China), ZEEKR (China), XPENG Inc. (China), and Rivian (US), among others. These companies have adopted strategies of new product development, expansions, collaborations, partnerships, and acquisitions to gain traction in the market. Collaborations were the most adopted strategy, among others.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=187205966