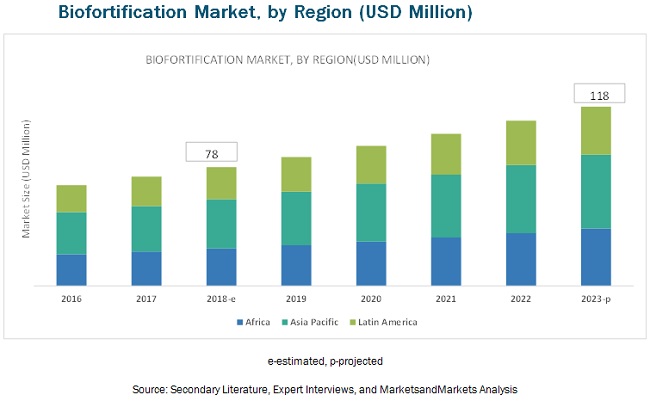

The biofortification market is estimated to grow at USD 78 million in 2018, and is projected to grow at a CAGR of 8.6% from 2018, to reach a value of USD 118 million by 2023. The growth of the biofortification market is driven by the rise in funds for agronomic practices and technological advancements. Biofortification is primarily used for the crops such as sweet potato, cassava, rice, corn, wheat, beans, pearl millet, tomato, banana, sorghum, and barley. The growth of the biofortification market is expected to be propelled by the increasing number of applications of biotechnological tools in plant breeding and farmers’ interests in increasing their farming investment for higher yield.

With advancements in biotechnology and genomic research, the application of biofortification for DNA selection is of prime importance, especially in plant breeding practices. The integration of this approach with conventional plant breeding practices led to biofortification processes; an interdisciplinary science that has immense opportunity for growth. Not only the rise in demand but also the fall in DNA marker costs is a major factor for the rapid adoption of techniques such as marker-assisted selection and genomic selection thereby boosting the growth of the biofortification market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38080924

Report Objectives:

- To define, segment, and project the global market size for biofortification

- To understand the structure of the biofortification market by identifying its various subsegments

- To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and industry-specific challenges)

- To analyze the micromarkets with respect to individual growth trends, future prospects, and their contribution to the total market

- To project the size of the market and its submarkets, in terms of value, with respect to the regions (along with their respective key countries)

- To profile key players and comprehensively analyze their core competencies

- To understand the competitive landscape and identify major growth strategies adopted by players across key regions

- To analyze the competitive developments such as expansions & investments, new product launches, mergers & acquisitions, joint ventures, and agreements

Sweet potato segment to dominate the biofortification market, by crop, in 2018

The sweet potato segment is estimated to hold the largest share of the global biofortification market in 2018. The demand for biofortified crops such as sweet potato and cassava has increased with the rising technological advancements to increase the nutrient content, particularly in orange-fleshed sweet potato (OFSP). Sweet potato is recognized as an important source of energy in the human diet for centuries owing to its high carbohydrate content. However, its vitamin A content from carotene only became recognized over the past century.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=38080924

Asia Pacific to be the dominant region in the biofortification market in 2018

The Asia Pacific is the dominant region in the biofortification market. Biofortification of crops has strong growth potential in agriculture, and it also improves the nutrition content in food. The biofortification market has grown considerably over the last five years, and this trend is expected to continue in the near future. The growing consumer demand for high nutritional content in food is projected to fuel the demand for biofortified crops, globally. Since the last decade, many countries in the Asia Pacific region have banned the usage of GM technology, and the researchers are opting to adopt biofortified crops as a key to unlock the region’s food production.

This report includes a study of marketing and development strategies along with the product portfolios of the leading companies in the biofortification market. It also includes the profiles of leading companies such as Bayer (Germany), Syngenta (Switzerland), Monsanto (US), and DowDuPont (US).